Introduction

Net Asset Value (NAV) is a core concept for anyone investing in mutual funds, exchange-traded funds (ETFs), closed-end funds, or other pooled investment vehicles. At its most basic level, NAV represents a fund’s per-share “book value”—the total value of its assets minus any liabilities, divided by the number of outstanding shares.

Knowing how NAV is calculated, why it changes, and how it is used can help you make more informed decisions as an investor. This guide covers all the essentials: from the formal definition and calculation steps, to how to evaluate funds based on NAV, and common strategies for maximizing your gains.

Whether you are a beginner just starting out in mutual funds or an experienced investor analyzing closed-end fund discounts, this glossary-style resource will walk you through everything you need to know about Net Asset Value (NAV).

Table of Contents

What Is Net Asset Value (NAV)?

Definition

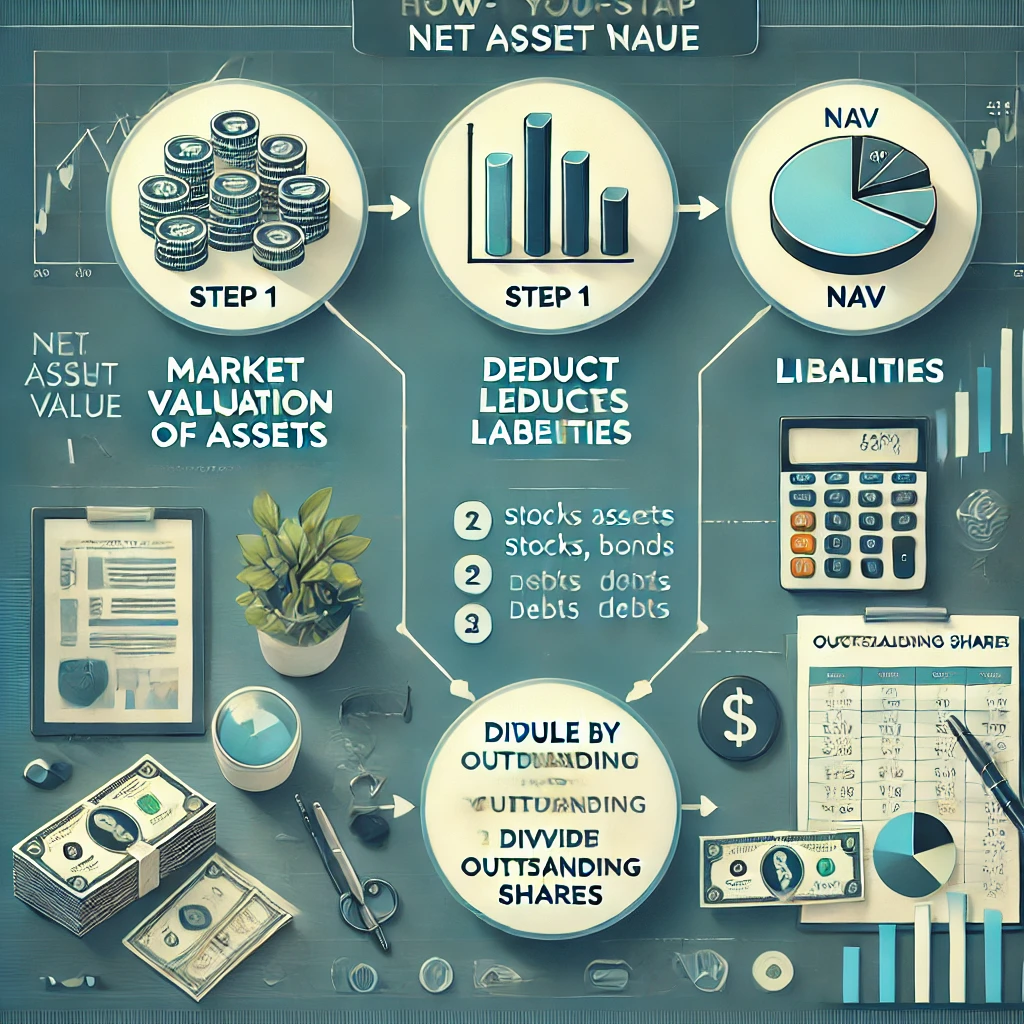

Net Asset Value (NAV) is the per-share value of a fund’s assets minus its liabilities. More formally:

NAV = (Total Assets – Total Liabilities) / Number of Outstanding Shares

- Total Assets: This generally includes all cash holdings, stocks, bonds, and any accrued income (dividends, interest) within the fund’s portfolio.

- Total Liabilities: These are obligations such as borrowed capital, operating expenses, and management fees owed but not yet paid.

- Outstanding Shares: The total number of fund shares currently owned by investors.

For open-end mutual funds, the NAV is the price you pay (or receive) when you buy (or sell) shares. As the SEC explains, open-end funds issue and redeem shares based on investor demand, so the NAV is recalculated every trading day after the market closes. This ensures that all investors who transacted on that day get the same fair price.

Primary Function

- Transparent Pricing. Unlike stocks, whose prices fluctuate throughout the trading day, most mutual funds price shares only once per day, using NAV as the standardized metric.

- Daily Valuation. At the end of each trading session (e.g., 4:00 p.m. ET in the U.S.), fund managers total up assets, subtract liabilities, then divide by shares outstanding to publish the official NAV.

- Investor Fairness. Because each day’s new investors and redeeming investors trade at the same daily-closing NAV, no one is penalized (or favored) by intraday market movements.

How Does Net Asset Value (NAV) Work?

The NAV Calculation Process

- Market Values. The fund’s portfolio is “marked to market” daily. For instance, if a fund holds 50 different stocks, each stock’s closing price is used to calculate total equity value.

- Add Accrued Income. If the fund is owed interest from bonds or dividends from stocks, these accruals are included in total assets.

- Subtract Liabilities. Management fees, administrative costs, and any borrowed money or accounts payable come out of the total asset figure.

- Divide by Share Count. The final figure is split across the number of outstanding shares, resulting in the day’s Net Asset Value per share.

Key Mechanisms

- Open-End Funds. Mutual funds are typically open-end vehicles that constantly create new shares to meet investor purchases and redeem existing shares when investors sell. As a result, the fund itself is priced only once per day at the official NAV.

- Closed-End Funds. With a closed-end fund, shares trade on an exchange. The market price can be above or below NAV, meaning investors might purchase shares at a discount or premium. Despite the market-determined price, the fund’s daily NAV is still published as a reference.

- ETFs (Exchange-Traded Funds). Like closed-end funds, ETFs trade intraday. However, ETFs typically remain close to their NAV through arbitrage mechanisms. They also publish an official end-of-day NAV, as well as an intraday indicative NAV (iNAV) that updates every few seconds or minutes. Check Fidelity or your broker’s platform for real-time ETF data.

Important Nuances

- Timing. Generally, if you place your mutual fund buy or sell order before 4:00 p.m. ET, you get that day’s NAV. Otherwise, you get the following day’s NAV. This rule helps prevent late trading abuses.

- Accrued vs. Distributed Income. Dividends or interest owed but not yet paid out is included in assets, boosting NAV. However, when distributions occur, NAV typically drops by the payout amount.

- Expenses and Fees. Fund expenses steadily reduce NAV. Over time, high expense ratios can have a significant negative impact on returns, especially when compared with similar funds offering lower fees.

Key Features of Net Asset Value (NAV)

Pros and Cons in One Table

Essential Details

- NAV vs. Market Price

- In open-end funds, NAV is the actual transaction price.

- For closed-end funds, the market can price shares below (discount) or above (premium) NAV.

- Distribution Impact

- When a fund pays dividends or capital gains, its NAV typically falls by the payout amount. Investors get the difference in cash or can reinvest automatically.

- A declining NAV after a distribution is not necessarily negative; investors retain total value via the combination of remaining NAV plus the distribution.

- Long-Term vs. Short-Term Focus

- Many day-to-day changes in NAV reflect broad market swings.

- For a long-term investor, total return (NAV changes + distributions) is usually more important than daily NAV moves alone.

How to Get Started with Net Asset Value (NAV)

Steps for Opening/Using an Account

- Research Suitable Funds

Look at historical performance, distribution history, and expense ratios via Fidelity, Investopedia, or your brokerage’s fund screener. - Open a Brokerage Account

Brokers like Fidelity, Charles Schwab, Vanguard, or TD Ameritrade provide user-friendly platforms to buy and sell mutual funds and ETFs. - Review Fund Expenses

The annual expense ratio is deducted from the fund’s assets. Even a seemingly modest 1% annual fee can substantially reduce long-term returns compared to a similar fund with a 0.50% fee. - Check Cutoff Times

For most U.S. mutual funds, you must submit your order before 4:00 p.m. ET to get that day’s NAV, per SEC regulations.

Rules and Restrictions

- Regulatory Requirements

Funds in the United States operate under the Investment Company Act of 1940, which mandates daily NAV calculations and standardized reporting. - Tax Implications

- Dividends and capital gains are taxable events in taxable accounts.

- Check IRS.gov for guidelines on reporting fund distributions and capital gains.

- Redemption Fees

Some funds charge short-term redemption fees if you sell within a specified timeframe. This lowers your realized proceeds, effectively reducing the NAV you receive.

Legal and Tax Considerations

- Prospectus Disclosures

Read a fund’s prospectus for details on how NAV is calculated, updated, and distributed. - State and Federal Laws

Certain states or countries may impose additional requirements or disclosures beyond federal rules. - Tax-Efficient Funds

Funds labeled “tax-managed” often attempt to minimize distributions, which can help keep NAV more stable and reduce your current-year tax burden in taxable accounts.

Examples & Strategies for Using Net Asset Value (NAV)

- Mutual Fund Investing

- For a long-term retirement account, daily NAV changes matter less than the fund’s growth and distributions over time. Evaluate total returns, not just raw NAV.

- Compare two funds with similar investment objectives by looking at how their NAV has grown over multiple years—especially including dividend reinvestments.

- Closed-End Fund Discounts

- Closed-end funds frequently trade at a discount or premium relative to their NAV. A discount may provide an opportunity if the fund’s fundamentals are strong; a premium indicates higher demand or a limited share count.

- Research thoroughly on sites like Motley Fool or Forbes to understand the reasons for persistent discounts/premiums.

- ETFs and Intraday Arbitrage

- Although ETFs have a market price changing second by second, they also publish intraday indicative NAV (iNAV). If the market price deviates too far from iNAV, large institutional traders can exploit that arbitrage, pushing the ETF price back toward its NAV.

- Tax-Loss Harvesting

- If a mutual fund pays a large distribution (and the NAV drops), you might use that time to sell other losing positions and offset gains. Always consult official IRS guidelines and/or a tax advisor to avoid wash-sale rule violations.

- Rebalancing Strategies

- Keep tabs on how each fund’s NAV grows. If it exceeds your target allocation, sell some shares and reinvest in underrepresented asset classes to maintain your ideal portfolio balance.

Frequently Asked Questions (FAQ)

1. Is a higher Net Asset Value (NAV) always better than a lower NAV?

No. A high NAV might simply indicate the fund has existed longer or accumulated more unrealized gains. A newer fund could have a lower NAV but still deliver excellent returns going forward. Always look at performance records, expense ratios, and distribution practices rather than just the raw NAV number.

2. Why does NAV change every day?

The value of the underlying assets (stocks, bonds, etc.) fluctuates daily due to market movements. Each evening, fund managers recalculate the total asset value minus liabilities. This update is the new daily NAV that investors see the following day.

3. How can I buy or sell shares at the day’s NAV?

In the U.S., if you place your mutual fund order before 4:00 p.m. Eastern Time, you’ll receive that same day’s NAV. Any orders placed after the cutoff will be processed at the next trading day’s NAV, as per the SEC’s rules.

4. Do expense ratios directly affect NAV?

Yes. Expense ratios reduce a fund’s assets, thereby lowering its NAV over time. For instance, a fund with a 1% annual expense ratio deducts these costs daily or monthly, affecting the NAV you see in your account balance.

5. What if a closed-end fund’s market price is different from its NAV?

Closed-end fund shares can deviate from the daily NAV due to market supply and demand. A discount might be an opportunity if you believe the market undervalues the fund’s holdings. A premium suggests investors are willing to pay more than the stated per-share net asset value.

6. Is NAV relevant for individual stocks?

Not usually. While you can consider “book value per share” for a single company, NAV is specifically used for pooled vehicles such as mutual funds, ETFs, and closed-end funds. Individual stocks trade based on market expectations, not a once-daily net asset valuation.

7. Can NAV be negative?

In almost all practical scenarios, no. A negative NAV would indicate a fund’s liabilities exceed its assets, effectively meaning insolvency. Regulatory safeguards and fund management practices make this extremely rare.

8. How does NAV work in private equity funds?

Private equity funds also calculate a sort of NAV for reporting. However, since private equity valuations aren’t determined by daily market prices, the reported NAV can be less transparent and updated quarterly or semi-annually. This makes private equity NAV somewhat more subjective.

9. Why do my fund statements show “unrealized gains”?

Unrealized gains are increases in the value of the fund’s holdings that have not been sold. They are part of the fund’s total asset base, contributing to the NAV. Once the fund sells those assets, the gains become realized, typically leading to distributions.

Conclusion

Net Asset Value (NAV) is a cornerstone of how mutual funds, ETFs, and many other pooled investment vehicles are valued and traded. By outlining the total assets minus liabilities on a per-share basis, NAV:

- Ensures daily transparency for investors

- Helps maintain fairness in open-end fund transactions

- Acts as a reference point for closed-end funds and ETFs

- Informs strategic choices around distributions, fees, and tax planning

For long-term investors, daily NAV swings may be less critical than total returns and the fund’s overall strategy. But whether you aim to spot discounts in a closed-end fund or simply want to understand how your mutual fund’s price is set, having a firm grasp of NAV helps you navigate the investing landscape with clarity.

When combining NAV knowledge with smart due diligence—reviewing SEC filings, checking a fund’s record on Fidelity or Investopedia, and monitoring expense ratios—you’re better equipped to make sound financial decisions. Over time, this understanding can be the difference between haphazardly selecting funds and building a portfolio designed to meet your personal and financial goals.